On a Shoogly Peg: CRV-cvxCRV

The plaguing pegging case of cvxCRV

Photo by Piret Ilver on Unsplash.

Abstract

The commission of veCRV is an ingenious model for Curve to coalign its token emissions with the future benefit reapable by the users (or vote-lockers). To put it simply, the users have their interests invested long-term in the Curve ecosystem. CTs throw around words like Curve War to describe the fight by different protocols to acquire the scarce CRV/ veCRV at their disposal for various distinct reasons. As the war evolved, multiple Legos have been developed to leverage the position of CRV/ veCRV for the metagovernance possibilities on the grander scale of liquidity battlefield beyond Curve. Amongst all the contenders, Convex has emerged victorious as the pack leader who has managed to accumulate the largest portion of veCRV thanks to its innovative disaggregation of yield and voting power in the form of cvxCRV and vlCVX, respectively. We think that the tokenomics design of Convex is brilliant, albeit some obvious challenges need to be addressed - as we explored them here, specifically regarding the issuance of cvxCRV.

P.S. all data points are valid at the time of writing on 9/3/22 at 20:00 (+8 GMT).

CurVE-tokenomics

This article assumes that the readers will have already been introduced to Curve and developed a basic understanding of the protocol's inner workings. For those who might need a refresher, we suggest reading the posts by @tokenbrice, @yuga.eth, and @nateliason, which they have made a pretty good coverage on the Curve protocol.

In short, Curve is a decentralized automated market maker which deploys:

a brilliant StableSwap invariant model for effective and low-slippage cross-market exchanges of stablecoins, and,

an ingenious vote-locking tokenomics (or ve-tokenomics) to allow the users to dictate the future token emissions. *Although we argue that this is not something new in the space in our previous submission, here.

Liquidity is the backbone of decentralized finance (DeFi). The very existence of liquidity allows the token owners to trade their holdings and subsequently seed the foundation of decentralized financial services. The two aforementioned features of Curve have effectively established a moat, which propels it to be the biggest protocol in DeFi with total value locked (TVL) in excess of $19 billion.

On Curve, the liquidity providers (LPs) are incentivized to accrue CRV, vote-lock them into veCRV so that they can boost the overall annual percentage yield (APY) for their liquidity position - and earn more CRV as boost rewards to increase their boostable portion. This phenomenon is often described as the flywheel effect by your friendly neighborhood Crypto Twitters (CTs).

The figure below should be pretty self-explanatory. As an LP, you could maximize your rewards by:

depositing either token of the relevant pool pair into the liquidity pool,

staking the LP token on Curve,

locking up a sufficient amount of CRV as veCRV (calculable here), and then

voting on the gauge weight for the pool containing your deposited liquidity to get a maximum of 2.5x boost for your share of CRV emissions and trading fees.

How Curve Works by Incentivized (yuga.eth) on Substack.

No vex, Convex is here

The formula above sounds gangsta-ish straight, outta the playbook of whales because essentially, they are the ones who could practically benefit the most from the system. With a considerable amount of capital at their disposal, they are more likely to possess a matching amount of liquidity and voting power in terms of veCRV to place themselves in a relatively comfortable position to farm more and more CRV. Don’t get us wrong; we have nothing against the whales because all minnows, dolphins, and whales are just individuals possessing different levels of wealth - bad actors exist irrespective of where they are placed in the wealth spectrum. The main takeaway is that the environment is not exactly friendly for the small players, which creates a lucrative market gap for the brilliant builders in the space.

Convex is here to save the day. It’s built to have a symbiotic relationship with the Curve. By introducing segregation between governance and returns on veCRV, the protocol quickly gained steams amongst the users. So now, CRV holders without providing liquidity or LPs without having veCRV to vote can maximize their earnings by using the facilities provided by Convex. The dynamics are described briefly below:

depositing either token of the relevant pool pair into the liquidity pool on Curve, and stake the LP token on Convex, or

converting CRV to cvxCRV, then

provide liquidity into the CRV-cvxCRV pool on Curve, and stake the LP token on Convex, or

stake it on Convex directly.

These two strategies showcase the win-win situation fostered by the introduction of cvxCRV. *And of course - CVX and vlCVX; but their synergy with Votium would not be discussed in this opinion piece to focus on cvxCRV solely. LPs could enjoy CRV emissions boost of approximately 1.7x and the share of their trading fee without needing to hold and vote with veCRV. CRV holders without liquidity can offer their governance voting power to Convex by getting cvxCRV in returns, allowing the holders to earn the usual rewards of veCRV plus other additional revenues.

In short,

On Curve,

LP without veCRV - basic trading fee for the specific LP and 1x CRV emission.

veCRV without LP - 50% trading fee of all LP revenue on Curve.

LP with veCRV - basic trading fee for the specific LP, up to 2.5x CRV emission (assuming veCRV used to vote for the gauge for the deposited LP) and 50% trading fee of all LP revenue on Curve

On Convex,

LP - basic trading fee for the specific LP, ~1.7x CRV emission, and CVX.

cvxCRV - 50% trading fee of all LP revenue on Curve, 10% of all LP revenue on Convex, and CVX.

The awkward position of cvxCRV

Apart from the perspective of earning more with literally the same amount of capital - by buying/ holding/ converting into cvxCRV instead of CRV, perhaps another noteworthy property of cvxCRV is that ones do not have to lock their CRV as veCRV for an exorbitant 4 years. cvxCRV can be exited back into CRV (despite the irreversible conversion process) via secondary markets of CRV-cvxCRV pool on Curve, Sushiswap, and Uniswap, respectively.

At first glimpse, cvxCRV is the celebrated brainchild for segregating the governance and yield aspects of the veCRV. In reality, there’s a creeping issue that has slowly become too big to be simply brushed off. The elephant in the room here is the growing negative premiums for the CRV-cvxCRV pool on Curve - as Curve holds the largest liquidity amongst the likes of Sushiswap and Uniswap (approximately $122.53 m in pool’s TVL versus $1.77 m and $ 0.05 m, respectively).

On Curve specifically, the pool now contains 12.42m CRV and 45.53 m cvxCRV, which brings the ratio of cvxCRV/CRV to be 78.57%. Trading 1 cvxCRV would only give you 0.9466 CRV back. The exchange rate of 94.66% for pegged assets is worrying because it translates to no conversion demand on Convex. At the current amplification coefficient of A as 50 - a 1 m token trade of cvxCRV to CRV would drop the rate to 94.20%, 5 m gives 91.44%, and 10 m returns an exchange rate of 83.56%, as shown here.

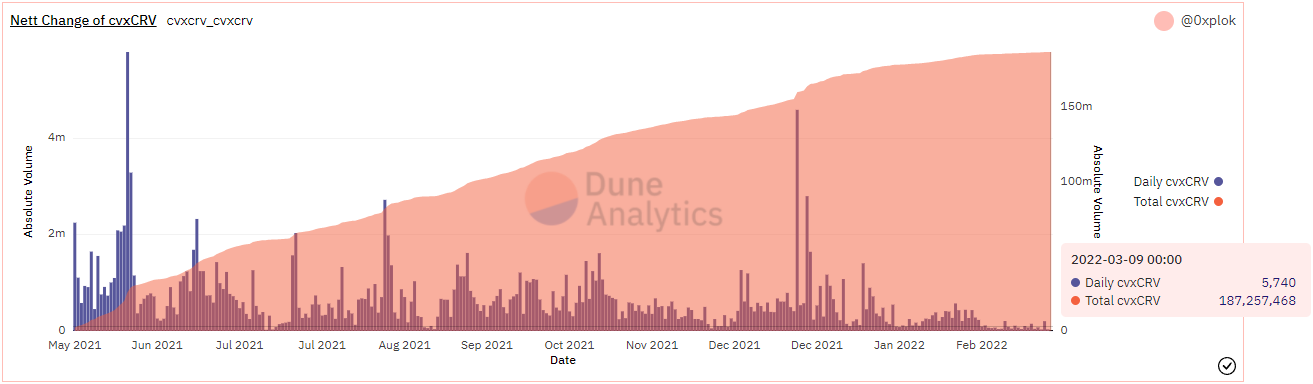

Coincidentally, the daily minting of new cvxCRV has decreased to a new record low starting from approximately mid-February, where an average of 200k cvxCRV were emitted to the circulation every day. This shows that fewer users are converting CRV to cvxCRV - which we hypothesized might be due to the current unfavorable market climate. However, this is not denying the very statement that the appeals of converting CRV to cvxCRV are decreasing for many DeFi participants. Not to mention, some of the new cvxCRV minted are the CRV fees returned to CVX stakers which get automatically locked in veCRV and tokenized as cvxCRV.

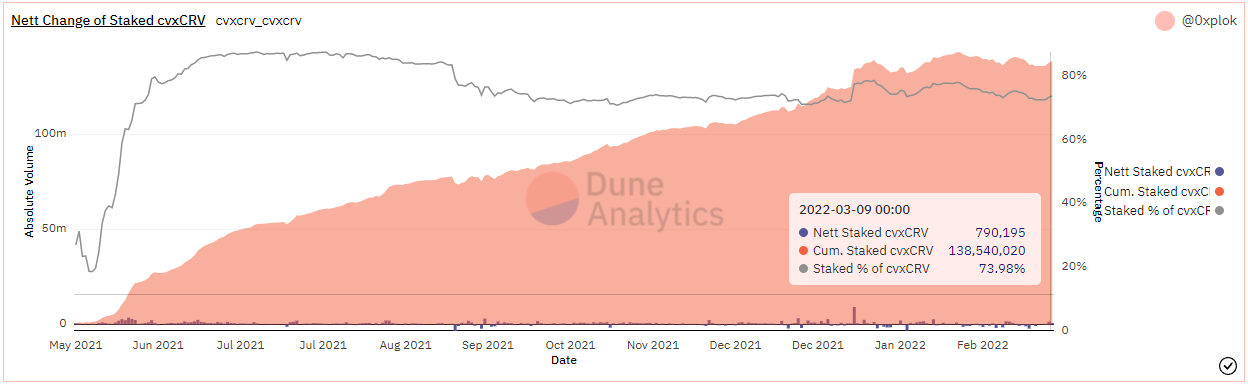

There are a total of 187.25 m cvxCRV in circulations, and around 138.54 m are staked - which is equivalent to 73.98% as the currently staked cvxCRV. Judging from the trendline of the staking graph, the staking % has not dropped drastically yet - which means the narrative of cvxCRV > veCRV in general still holds, albeit it’s only hovering around the lower range of 70ish %.

There’s a catch, nevertheless, which the emissions of CVX are coming to an end. As cvxCRV = veCRV + 10% Convex LP Fee + CVX, taking out CVX from the equation will strongly affect the yield prospect of holding cvxCRV.

Tl:dr, the bigger issues here are:

creeping negative premiums,

fewer cvxCRV get minted from organic CRV,

dipping ratio in the (largest) Curve liquidity pool, and

CVX emissions are coming to an end.

Closure

Anon, are you worried about all these findings? Perhaps, do you think the guy behind the screen is just writing this down to fud your bags? Well, all hopes are not lost in Gotham. There are plenty of efforts being initialized to tackle the core of these challenges.

One exciting protocol is the Union’s pounder by @0xAlunara, which effectively helps to auto-compound the rewards of cvxCRV (back) into cvxCRV, improving the peg of CRV-cvxCRV by allowing the users to stake and forget simply. Specifically, this protocol solves the pain point of users having to spend high gas fees to do the same thing manually. *The stats for the Union’s pounder are also available in the Dune dashboard.

Some suggestions floating around are to ramp up amplification coefficient, A to lower slippage and improve the peg (or exchange rate). (Play with the graph here!) However, we argue this is only a short-term fix if the suggestion is accepted. The leveraged bet on the price to revert to 1:1 has no basis to justify itself. Also, some of the generalized arguments of increasing A are presented below.

In our opinion, the long-term solution for this challenge lies in the yield equation of cvxCRV itself.

cvxCRV = veCRV + 10% Convex LP Fee + CVX

What if, there’s a new disruptive protocol to improve this equation and allow the users to earn more? Effectively, the health and longevity of Convex can be ensured as well.

cCRV = cvxCRV + ???

Stay tuned, anon.

Alpha-sharing on 10/3/22 at 21:00 (+8 GMT) in Congruent Discord.

Source:

All the aforementioned data points are retrieved directly from the Dune dashboard.

Disclaimer:

The author holds CRV, CVX, vlCVX and cvxCRV tokens. The opinions expressed in this article are those of the author’s and do not necessarily reflect the Congruent's official policy or position. They should not form the basis for making any financial decisions either.